英语

英语 西班牙语

西班牙语 中文简体

中文简体Beyond Cutting: How Nonwoven Abrasives Are Shaping the Future of Precision Finishing

1. Market size and growth trajectory

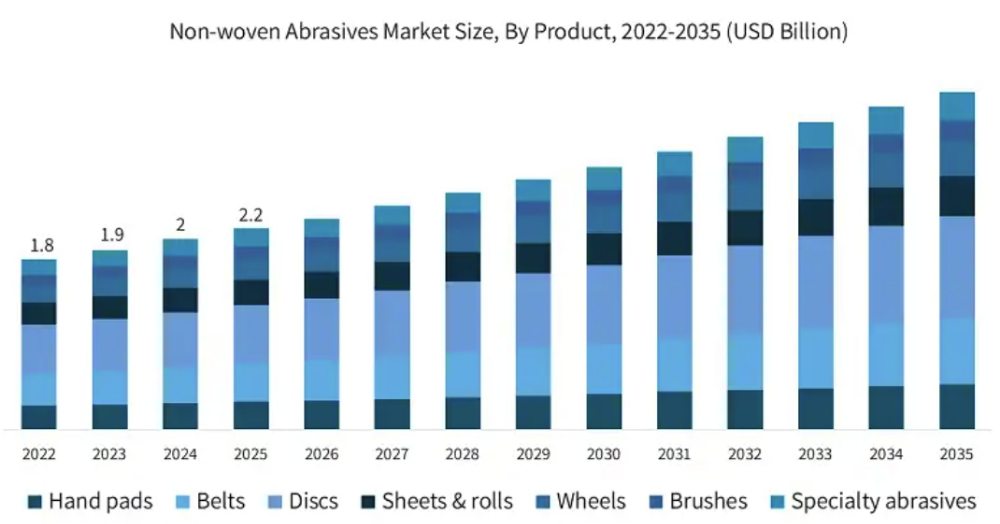

By 2025, the global nonwoven abrasives market is valued at approximately $2.2 billion. With manufacturing industries increasingly demanding surface quality, process stability and compatibility with automation, the market is projected to reach 2.3 billion by 2026 and grow to 3.6 billion by 2035.

Unlike traditional bonded or coated abrasives, nonwoven abrasives focus on controlled removal and consistent results. Its value lies not in raw cutting speed, but in its ability to maintain surface integrity, improve finish and deliver repeatable results. That is why they are gaining ground in precision manufacturing, automotive repair, the aerospace industry and high-end metalworking.

2. Technology trends: from "faster" to "smarter"

Recent innovations in nonwoven abrasives are less about speed and more about control.

Fiber Engineering: The use of micro fibers and engineered fiber blends allows the abrasive to conform to complex curves and irregular shapes without altering the geometry of the part. This enables a uniform finish even on intricate surfaces.

Abrasive minerals: The introduction of ceramic grains helps maintain stable cutting performance throughout the life of the product. Compared to conventional aluminum oxide, service life is typically increased by 40% to 60% – a critical advantage for automated lines and continuous processes.

Binder Systems: New resins and bonding agents are more resistant to heat and humidity, and increasingly environmentally friendly. These nonwoven products can operate reliably at 200–250°C, making them suitable for wet grinding, marine applications and heavy metal processing.

3D structured surfaces: Better chip evacuation and waste removal makes these abrasives very effective for grinding welds, heavy duty deburring and coating removal.

3. Main drivers and challenges

Drivers:

Automation and precision manufacturing: Robotic finishing cells and CNC systems require abrasives with predictable material removal and low risk of surface damage. Nonwoven products are becoming standard in these environments.

Advanced materials: Aluminum alloys, titanium, composites and high-strength steels – widely used in the aerospace and automotive sectors – are very sensitive to heat and surface damage. Field data shows that nonwoven abrasives can improve processing efficiency by 30% to 40% while significantly reducing heat buildup.

MRO (Maintenance, Repair and Operations): The growing installed base of industrial equipment around the world generates stable demand for versatile and easy-to-use abrasive products.

Challenges:

Raw material price volatility: Synthetic fibers, specialty resins and abrasive minerals are affected by energy and supply chain fluctuations. In periods of shortage, manufacturing costs can increase by 15% to 25%.

Competition from alternative technologies: Laser surface treatment, chemical etching, and high-end coated abrasives compete in some precision applications, particularly in electronic and medical device manufacturing.

4. Discs and grinding wheels: volume boosters

Among product forms, nonwoven discs account for approximately $625.8 million in 2025 – about 29% of the total market. Their ability to conform to curved surfaces and compatibility with various power tools make them the most cost-effective choice for finishing automobiles, stainless steel, and aluminum.

Nonwoven belts reach $410.3 million, with increasing adoption in automated finishing systems for deburring, chamfering and continuous surface treatment.

Nonwoven grinding wheels also sit at $625.8 million, serving high-end applications such as aerospace, automotive OEM and precision manufacturing, where consistency and stability are paramount.

5. Growth by grain size – a clear shift towards fine grains

The market shows a clear concentration towards fine grains.

Fine grain (180–600 mesh): Valued at $970.8 million in 2025, accounting for 45% of the total market share. They are essential for finishing and polishing, especially in clear coat blending, stainless steel polishing and decorative surface treatments – often the final step in the process.

Medium grit: $787 million, primarily used for deburring, surface preparation and finishing between processes. Demand is growing steadily with manufacturing expansion.

Coarse grain: $401.4 million, most common in heavy grinding and maintenance applications such as shipbuilding, industrial renovation and MRO.

6. Applications – cleaning, deburring and finishing, all growing

Surface cleaning and preparation is the largest application segment: $648.6 million in 2025, widely used for weld cleaning, pre-painting and pre-assembly treatment.

Deburring and edge rounding reaches $469 million, driven by the spread of CNC machining, laser cutting and robotic finishing systems.

Finishing and Polishing, although smaller at $180.5 million, has the highest added value in premium sectors such as medical devices, high-end decorative metalwork and aerospace.

7. Regional outlook – growth shifts to Asia-Pacific

North America and Europe remain important premium markets. In 2025, the United States alone represents $551.5 million, with demand coming mainly from the automotive, aerospace and advanced metalworking sectors.

The Asia-Pacific region is the fastest growing. Expanding manufacturing scales in China, India and Vietnam, along with growing local production capacity, are driving significant demand for nonwoven abrasives. Emerging markets like Saudi Arabia and Brazil are also seeing steady growth due to infrastructure development and industrialization.

8. The true competitive advantage: technology application knowledge

Overall, the nonwoven abrasives industry is moderately concentrated. The competition is not mainly about price, but about:

Fiber structure design capability

Abrasive mineral system stability

Product consistency and uniformity

Deep understanding of application scenarios

As customers demand more standardized finishing processes, certified quality and automation-ready solutions, companies that provide application engineering support – helping customers design their processes and offering long-term collaboration – will secure the strongest positions in the market.